Mortgage Refinance

Benefits of Refinancing Your Mortgage & What You Need to Know

Explore refinancing to potentially reduce your monthly mortgage payment with today’s lower rates, accelerate payoff with a shorter term, or tap into your home equity to fund renovations, payoff debt, or manage other large expenses

Why homeowners finance?

Mortgage refinance guidelines

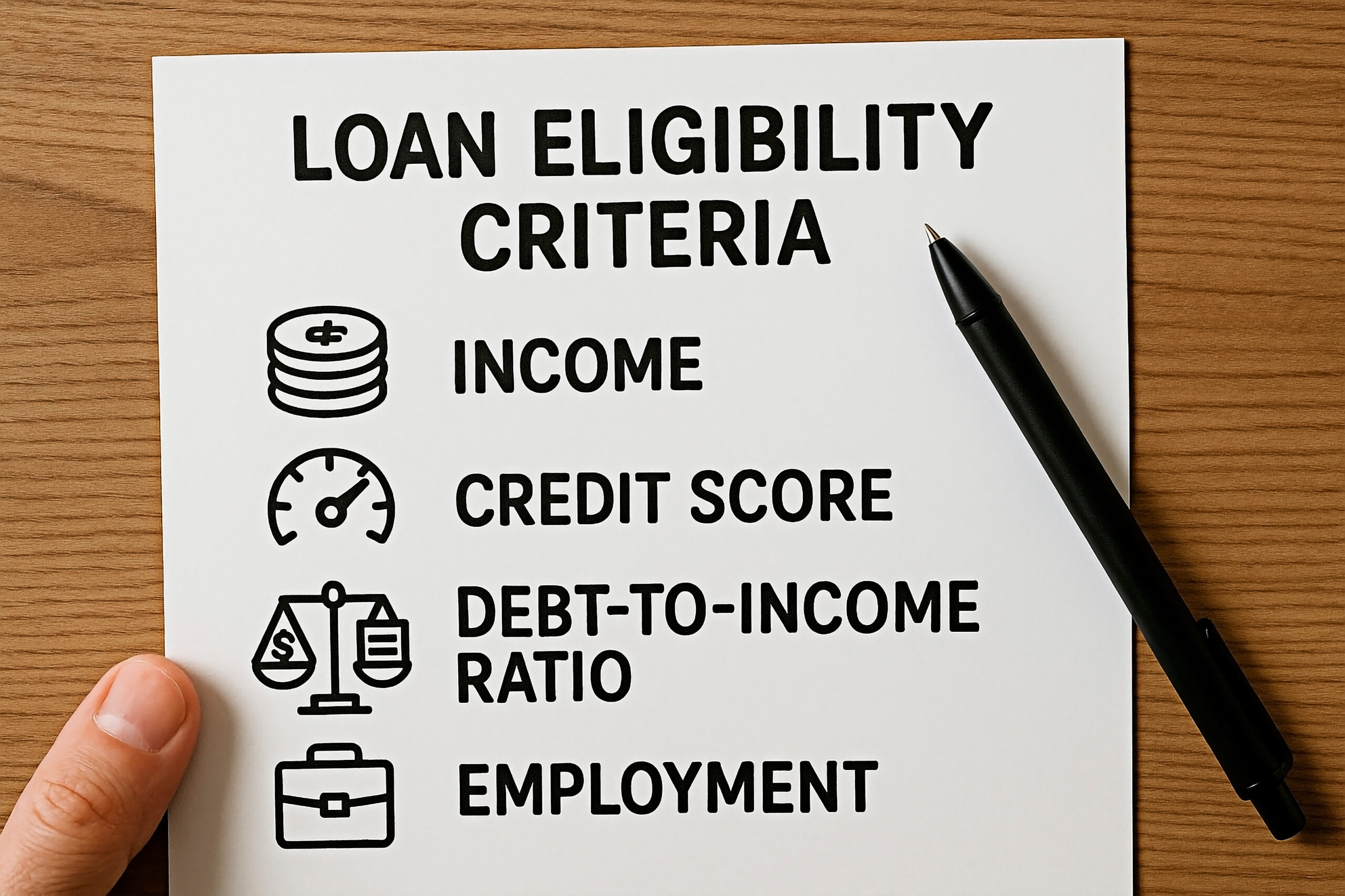

The qualifications for refinance depend on the mortgage program, but you could need:

To better understand your options and the guidelines its important to identify your existing mortgage and your goals. If you would like to cash out equity, the documentation requirements will be similar to your purchase. Refinancing may involve costs including underwriting, appraisal fees, title insurance, settlement fees that should factor into your decision – to help determine your break even. Learn more about your options below.

Overview of Mortgage Refinance Programs

Learn more about your mortgage refinance options

Refinance Calculator

Current Loan Details

New Loan Details

Start Refinance Application

What Our Clients Say About Us

Divide the total closing costs by your monthly savings from the new loan. Example: If costs are $5,000 and you save $200/month, it takes 25 months to break even. If you plan to stay in the home longer than that, it could save you money overall. Factor in total interest over the loan life — shortening the term saves interest but raises monthly payments.

Typical closing costs (excluding rate buy-downs and escrows/prepaids) are approximately $4,000 to $6,000 and cover appraisal fees, underwriting, title insurance, settlement fees, credit checks, appraisals, etc.

You are eligible to refinance after making 6 on-time payments and provided the rate is at least 1/2% lower than your current rate

You are not required to escrow on conventional, VA and non-qm mortgages (bank statement, PnL and DSCR). FHA requires escrows for taxes and insurance).

")